TERRA CARIBBEAN MARKET REPORT: Residential Sales | 2025 | Barbados

Terra Caribbean’s residential sales data for 2025 reflects a market that is stable in volume but stronger in value. The number of residential properties sold declined marginally by 2.4%, while total sales revenue increased by approximately 33%, supported by a 19% rise in average sale price. Growth was driven by higher-value segments, with 86% more properties sold above $2M increasing market share from 6% to 13%. Sub-$1M property sales declined by 10% but continued to dominate overall activity, representing 75% of all sales transactions. Ongoing increases in construction costs, alongside the mix of new higher-spec developments, have contributed to higher pricing levels.

Looking ahead, lead indicators remain positive, with sales enquiries up 34% in 2025 and pending sales still elevated, albeit easing slightly into 2026. Market activity continues to be driven by supply in key developments and strong foreign demand in higher price brackets, while pricing conditions remain stable with low average discounting and over half of transactions achieved at asking price. Overall, the data points to a resilient market entering 2026, with demand holding but increasingly dependent on the availability of quality stock across segments.

- Terra Caribbean recorded a 2.4% decrease in the number of residential properties sold in 2025 compared to 2024

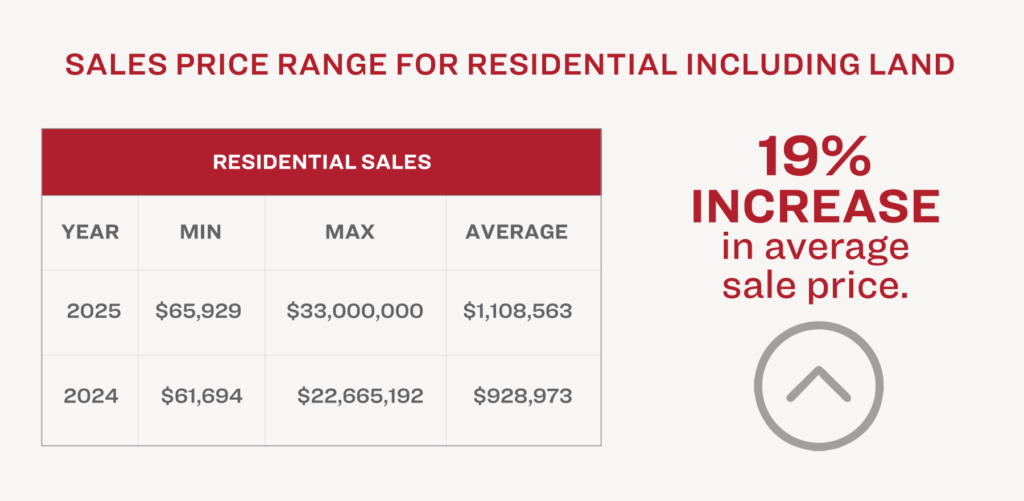

- Despite the reduction in transaction volume, overall residential sales revenue increased by 33%, supported by a 19% rise in the average sales price. The maximum sales values and average prices reported for both 2024 and 2025 exclude flagship property sales completed during this period.

- Sales of residential properties below $500,000 remained stable accounting for 44% of the market

- The $500,000–$1M segment reached a five-year high in 2024, driven by the completion of developments such as The Estates (St. George),Coral Beach (St. Peter), and new homes at The Villages at Coverley

- While this segment declined by 21% in 2025, activity remained well above levels seen during the 2000–2023 period, suggesting performance is closely linked to the availability of quality product

- Well-planned communities in this segment continue to attract a broad range of buyers, including young families, investors, foreign purchasers, and retirees, drawn by the value, security, sense of community, and convenience they offer

- Properties under $1M accounted for approximately 75%–81% of all sales in 2024 and 2025, underscoring sustained demand in this segment

- The $1M–$2M segment remained steady at 13% of the market

- Sales in the $2M–$4M range more than doubled with growth of 127%, supported by the completion of Allure on Brighton Beach—the first apartment development in this emerging area on the West Coast, which was fully sold prior to completion

- There was a 45% increase in sales in the luxury segment (over $4M), typically driven by foreign buyers. Much of this growth came from transactions above $6M

- There was a notable shift in buying patterns in this segment with off beach stand-alone homes comprising 81% of properties purchased above $4M, compared to 45% in 2024. This is being driven by a higher percentage of foreign buyers planning to spend longer stretches on the island with space to accommodate friends and extended family whilst here

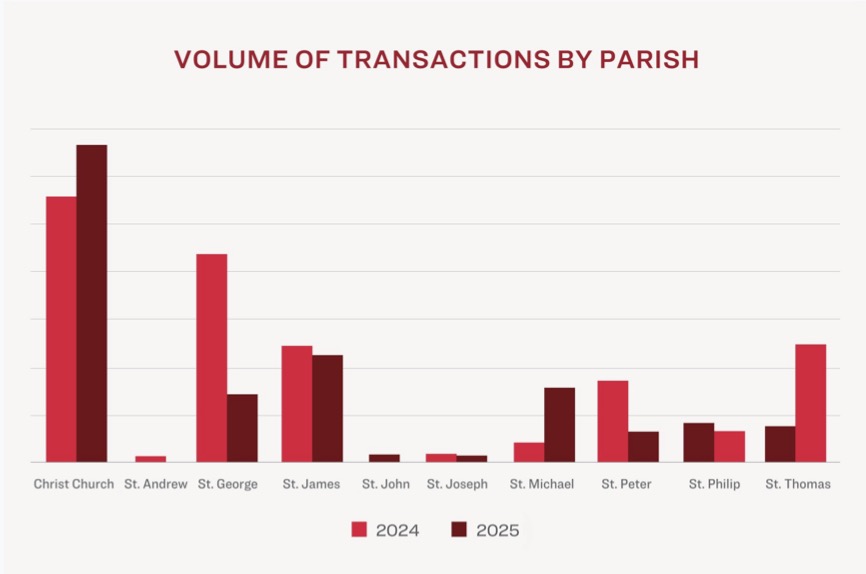

- Christ Church remains the core market, driven by mid-range housing and land sales, accounting for 42% of sales transactions in 2025 St. James and St. Peter, traditionally among the most active parishes, represented a combined 18% market share, with average prices increasing by 49% in St. James and 27% in St. Peter. St. James continues to dominate the luxury segment

- St. Thomas, typically a less active parish, captured a strong 16% market share, driven by the popularity of Sunset Views—a ridge-front land development in Dunscombe launched in mid 2024. The project offered 58 attractively priced lots starting at $100,000 and is now fully subscribed

- St. Michael’s market share increased from 2% in 2024 to 10% in 2025, driven by the completion of the popular Allure project, the first apartment building of its kind on Brighton Beach. This project offered 24 two and three-bedroom contemporary residences fully selling out prior to completion

- St. George moved from second to fifth position, as 2024 activity had been significantly elevated by bulk apartment closings at The Estates

- Activity in other parishes remained relatively stable, accounting for the remaining 6% of sales, with St. Philip contributing the majority of achieved sales within this group

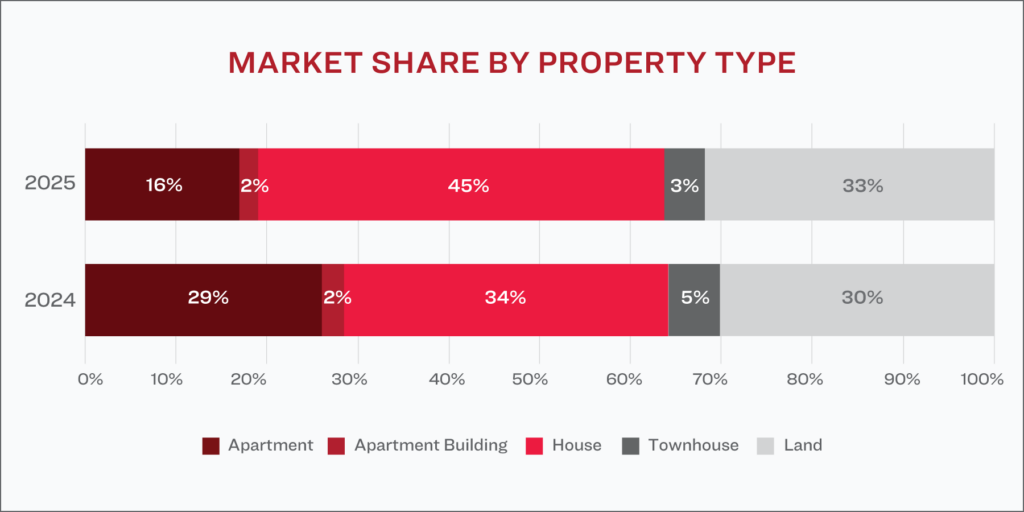

- Houses have consistently dominated the market in the post-COVID period, accounting for the largest share of sales transactions. This reflects both sustained buyer demand for houses and increased availability as developers cater to this demand

- In 2025, houses saw a notable uplift, increasing from 34% to 45% of total sales, bolstered by increased supply

- Land also saw modest growth, rising from 30% to 33% of sales transactions, indicating steady demand in this segment

- Apartments declined from 29% to 16%, while townhouses fell from 5% to 3%. These movements have been influenced, in part, by the underlying supply of available properties

- While the inventory of well priced apartment buildings is low this property type continues to be attractive to potential buyers accounting for 2% of the market

- Overall, the data reflects a market led by houses, with growth in land and softer activity in apartments and townhouses, shaped by both buyer demand and the types of developments being brought to market

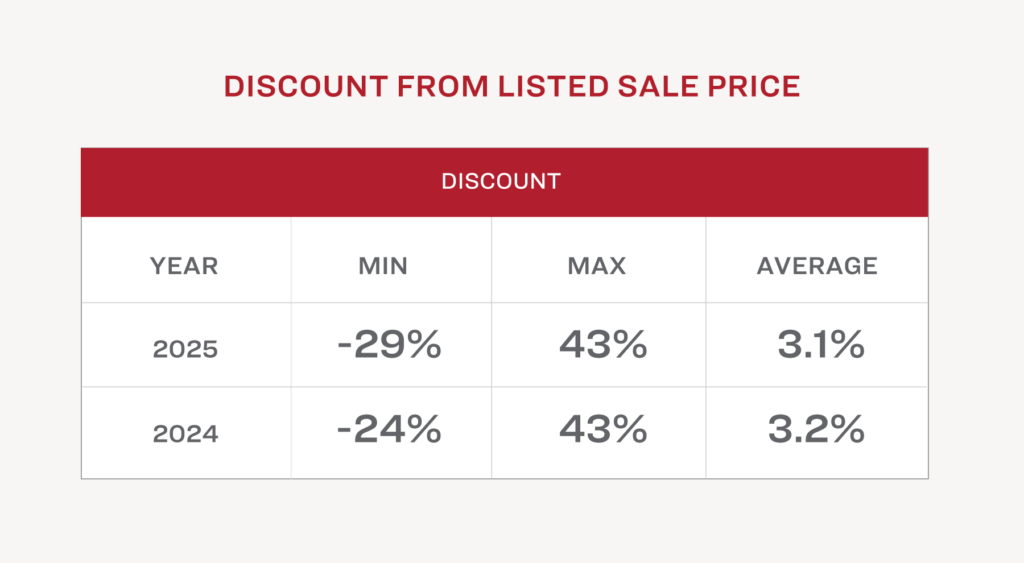

- Average discount levels between Listed Sale Prices and Agreed Sale Prices have remained steady after falling by 0.8% in 2024 remaining at their lowest level in five years

- Notably 54% of sales agreed at the listed price, suggesting list prices were well aligned with market demand

- Discounting, when it occurs, is typically modest, with 30% of sales closing 1%–10% below list price

- The largest discounts continue to be situational, mostly linked to forced sales or properties that were initially priced above market, rather than a broad-based softening.

- 3% of properties received simultaneous offers in both 2024 and 2025, resulting in agreed sale prices exceeding list price. In 2024, the highest premium was achieved for a well-located ridge front home with ocean views on a spacious plot in St. Peter, while in 2025, a sea view land parcel near the cliff front in St. Philip attracted the strongest premium

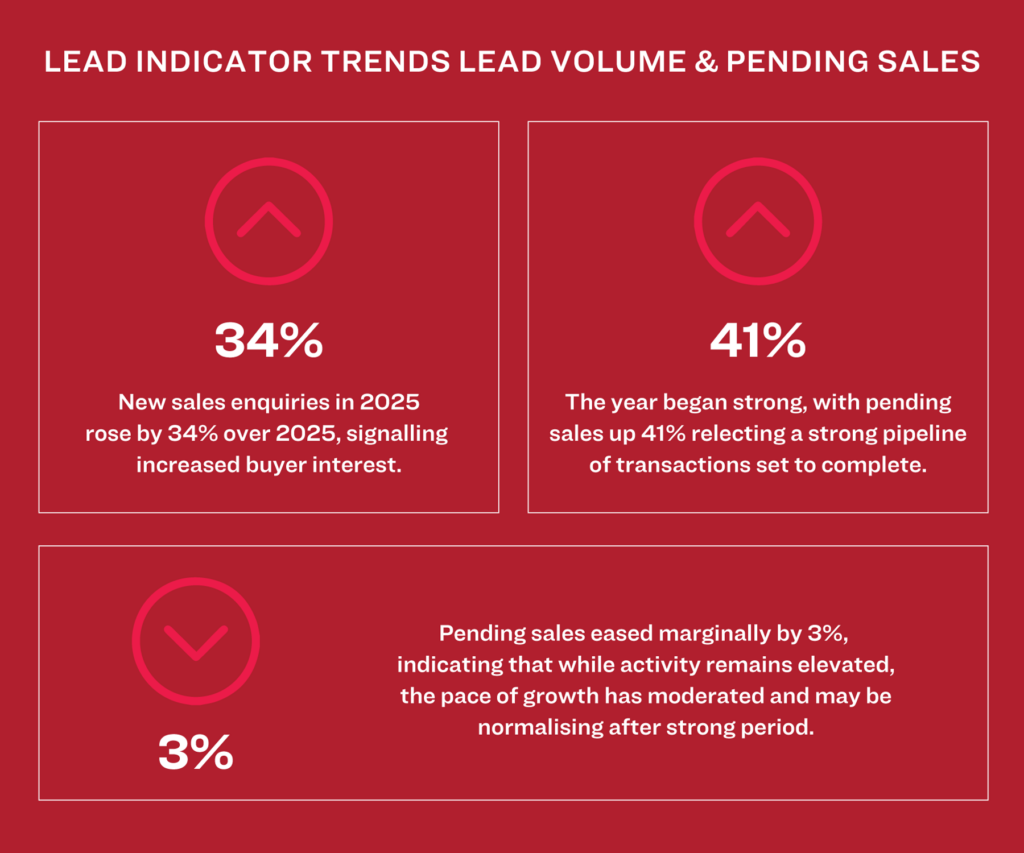

- New sale enquiries accelerated through 2024–2025, with sales enquiries rising 22% in 2024 and a further 34% in 2025, indicating sustained momentum in purchaser interest

- Forward activity remained robust entering 2025, with pending sales as at January 1st up 41% year-on-year, reflecting a strong pipeline of transactions set to complete

- Entering 2026, pending sales eased marginally by 3%, indicating that while activity remains elevated, the pace of growth has moderated and may be normalising after a strong period

- Overall, market conditions appear stable, with steady enquiry levels and a resilient pipeline, though both are likely influenced by the availability of stock as well as underlying demand

** Pending sales measures the value of sales agreed and awaiting settlement as at January 1st

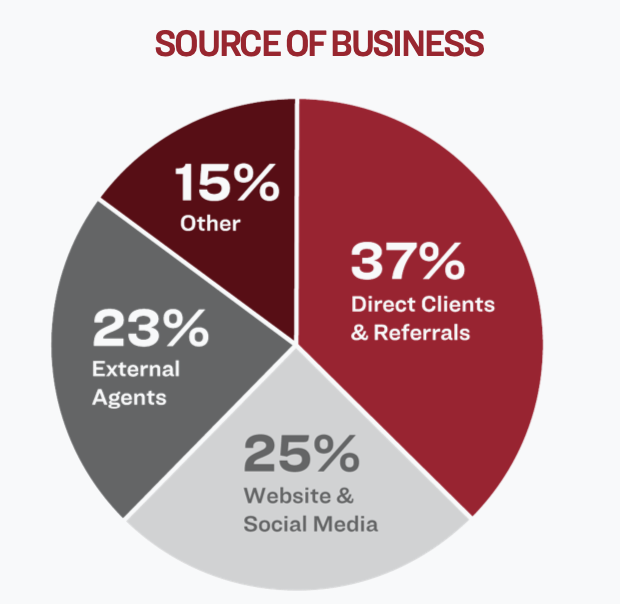

- Direct clients and referrals remain our strongest source of Sales & Rentals leads, contributing 37%—a reflection of the trusted relationships built by the team

- Websites & social media are the second strongest lead source (21%), underscoring the importance of digital channels

- Collaboration with other agencies accounts for 23% of our leads also plays a significant role highlighting valuable partnerships in the sector

- Events, signage, and other advertising channels account for the remaining 15%

- Overall, the distribution is in line with historic trends, indicating a stable lead mix